Ever since the interest rate trend reversal last year, financial mathematics has been a different game. Companies have been moaning about higher financing costs, banks have been expanding their interest margins but have also had to increase provisions. By contrast, business has been buoyant for the independent financial broker Compagnie Financière Tradition, which is headquartered in Lausanne. The stock impresses with its steady performance and attractive valuation.

CFT does not often make the headlines. This might have something to do with the discreet nature of its fundamental business. CFT is the global number 3 in what is known as the interdealer-broker business. These are brokers that only have business relationships with professional dealers, and bring together supply and demand for commodities, financial instruments, derivatives, options, as well as other assets traded in (or outside of) the over-the-counter (OTC) market. The market position of CFT is outstanding. Thanks to its strong balance sheet, in which shareholders’ equity makes up 41.5% of total assets, the company is a winner in the process of consolidation within the interdealer-broker segment. Its two key competitors – TP ICAP and BGC Partners – have weaker balance sheets, while smaller players are increasingly feeling the pressures of regulatory and technology requirements.

The market for exotic, illiquid and critical trades

The potential volume is huge, but the individual items traded are very specific, often with very low liquidity and only of interest to specific customer groups. Things like interest rate swaps, commodity forward contracts, and crude oil and electricity supply contracts are only interesting to very specific market participants such as energy suppliers and manufacturing companies, for example. It is also not a rarity for positions in certain government or corporate bonds, equities, or derivatives to be too large not to have an impact on securities exchange pricing or not to raise questions. This is where the company’s longstanding network of contacts with industry, dealers, and a variety of financial market players – as well as its presence in 30 countries from Argentina to South Africa and China – with a workforce of some 2,300 comes in useful. The number of its clients rose by 2.8% in 2022 to 582,500.

Low-risk business model

While this business area might sound highly speculative, CFT has developed a risk-averse and solid business model characterized by flexible cost structures, a scalable platform, and healthy margins. The bedrock of the business is the fact that the items traded do not get taken onto the company’s own books – CFT does not engage in proprietary trading. It acts purely as a broking agent, i.e. as a “matchmaker” between parties. In other words, it is not exposed to price risks that could lead to shareholders being held liable in the event of loss. Almost all of CFT’s revenues take the form of commissions, which means it profits from rising business volumes – much like in the 2022 financial year.

Cyclical and structural surge in demand

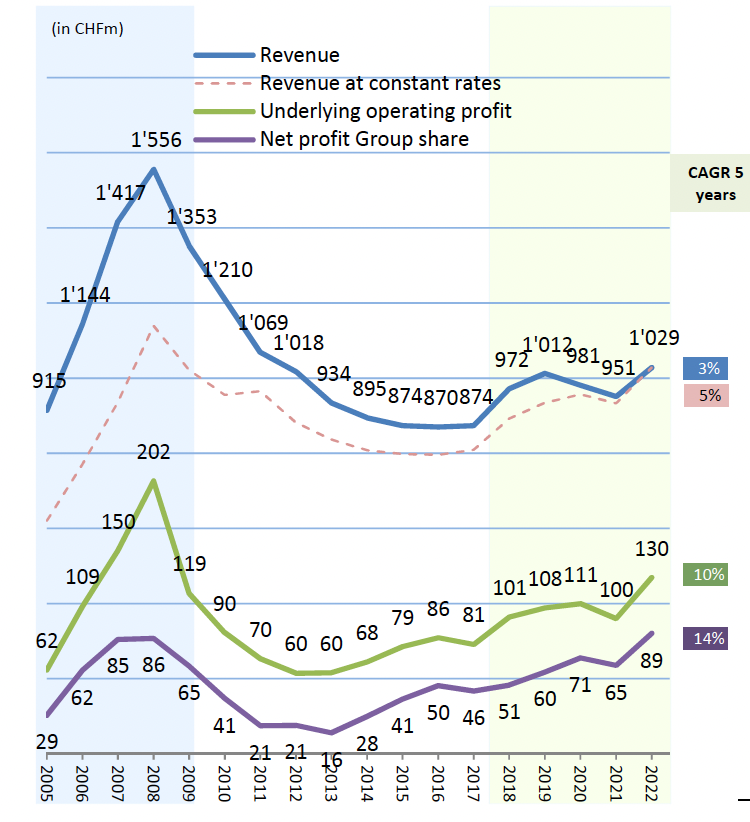

Revenues rose by 10.5% in 2022 to CHF 1.03 bn. Growth proved strong in all regions, with revenue increases ranging from 9.5% in Europe to 12.8% in the Americas. North and South America together account for 31% of revenues, followed by the UK (28%), Asia-Pacific (27%), and Continental Europe (14%). Business development is influenced by a number of factors, both cyclical and structural. The most important of these are macroeconomic trends, commodity cycles, volatility, emerging markets, budget deficits, the interest rate environment, and the issuance of government and corporate bonds.

Growth drivers

A number of different growth drivers can currently be discerned. The investment managers Manuel Bottinelli and Adrian Lechthaler of wealth manager Peter J. Lehner & Partner AG in Zug summarize these as follows: “The increase in financial market volatility and the adjustment to asset class weightings due to changes in interest rates have brought about a structural improvement in the market environment for CFT. The return of workers to the office is also playing a role, as ultimately this is a people business. From a competitive perspective the ongoing process of market consolidation is worthy of note, as CFT will probably emerge as a winner from this.”

Profits surge in 2022

CFT is an efficient business due to a lean and flexible cost base along with active management of company-wide structures such as IT, Compliance and Risk, Legal and Human Resources, and Accounting and Finance. Net profit after minorities – joint ventures account for CHF 81.2 million of revenues – increased to CHF 89.1 million, which equates to a 40.3% rise on the somewhat weaker prior-year figure. This has in turn lifted earnings per share to CHF 11.83, up from CHF 8.76 the previous year. After five years of an unchanged dividend, the recent AGM approved the proposed 10% increase to CHF 5.50 per share for the 2022 financial year. In addition, shareholders are to receive one new share for each 100 shares held by way of a stock dividend.

The long-term view

CFT was founded back in 1959. Following the sale to the French company Groupe Pallas, current majority shareholder Patrick Combes took over control of the company in the mid-1990s. Thereafter, CFT was expanded through the establishment of subsidiaries, but also by takeovers and joint ventures. A longer-term view reveals that business volumes embarked on a sharp upward trajectory right up to 2008. In the year that saw the onset of the financial crisis, revenues reached a record level of CHF 1.56 bn, with profit amounting to CHF 86 mn. However, the subsequent slashing of interest rates globally and the bond-buying programmes of central banks resulted in an erosion of the company’s business for the best part of a decade, with annual revenues at hitting a nadir of CHF 870 million in 2016/2017.

Management performance

It is to the credit of management that the low point of profitability (CHF 16 mn) was recorded as early as 2013 – with a rising trend ever since. The margin has gradually improved to 8.9%. This trend is attributable to business optimization through technology, operating management, and increased cost efficiency. But the latest paradigm shift came in 2022, when a variety of factors simultaneously provided significant stimuli to CFT’s business – the interest rate trend reversal, rising price trends for commodities and energy, and higher financial market volatility. In particular, interest-rate instruments and products enjoyed a substantial surge in demand in 2022, which has persisted into the current year.

The boon of rising interest rates

The shift from “QE” to “QT” and higher interest rates will probably continue to trigger volatility and dislocations in the financial markets. To this extent, the reversal of expansionary central bank policy and the new focus on combating inflation is providing CFT with a strong tailwind that could yet morph into a thermal wind. The language of central bankers is becoming ever clearer, with German Bundesbank President Joachim Nagel recently quoted at a conference saying: “We haven’t yet slayed the inflation beast.” This does not sound like a short-term or simple undertaking. For CFT, the process of monetary trend reversal could in the best scenario result in a pattern of business similar to that experienced prior to the financial crisis of 2008/2009.

FX platform in Japan

In addition to the cyclical forces driving business development, there are also opportunities arising for the company from structural change. One example is the gaitame platform in Japan, which executes forex transactions rapidly and cost-efficiently as a result of digitalization. Unlike all the company’s other business areas, this platform was conceived for retail clients. The corresponding revenues rose by 14.6% in 2022 to CHF 33.9 mn. More pleasingly still, the EBITDA margins for this business work out at around the 50% mark, making the platform already a significant contributor to earnings. Further growth is anticipated, as peer-to-peer transactions in the foreign exchange market have so far achieved only a very low level of market penetration.

Joint venture in China

Another example of a structural driver is the joint venture Ping An Tradition in China. Partner Ping An is one of the world’s largest insurance companies, with a current market capitalization of USD 127 billion and numerous activities in the worlds of investment and banking. Out of a workforce of more than 300,000 employees, more than 20,000 work in IT, where artificial intelligence is a key focus. In its Annual Report, CFT stresses that Ping An Tradition has played a significant part in the success of its joint venture activities. Its pre-tax earnings contribution rose by 31% in 2022 to CHF 29.6 mn.

Dividend continuity and outlook

At 4.6%, the dividend yield is already more than acceptable. However, despite the 10% increase, the payout ratio has dropped to 47%, the lowest level on record. A strong equity ratio and plentiful liquidity are now also allowing the company to implement a share buyback programme. According to the corresponding AGM resolution, 300,000 shares are to be bought back and then cancelled by May 2026. As a result, company earnings going forward will be split between fewer shares. Professional investors Lechthaler and Bottinelli, who hold a long-term position in the stock for their clients, view the company’s dividend policy and performance in a very positive light: “Since 1997, CFT has paid out some CHF 127.50 [per share] in dividends, quite aside from the free shares. The total return on the stock since 1997 works out at an impressive 17% p.a., which compares to 6.5% and 6.8% for the SMI Index and the SPI Index respectively.”

Outlook

The decisive event in 2002 was the interest rate turnaround after 15 long years dominated by low-interest monetary policy and QE. This has given a substantial boost to the interest rate business that is so important to CFT, and given the persistence of core inflation this theme is likely to remain an important driver going forward. The company’s commodity and energy business has also been thriving. Financial market volatility is good for CFT’s business generally. Moreover, the company is ideally positioned to take advantage of the growing importance of emerging markets given its subsidiaries and joint ventures around the globe. Further growth stimuli are coming from the process of consolidation in the interdealer-broker segment. Last but not least, Bottinelli and Lechthaler see a further potential catalyst: “CFT has a highly profitable and fast-growing data business with machine learning algorithms, which is somewhat under the radar and therefore not really reflected in the stock price. With a change in perception, there is attractive re-rating potential here.” That said, there are also risks. An obvious one that springs to mind is key individual risk, as the success story of CFT is to a significant extent bound up with the work of the majority shareholder over a period of several decades. Viewed in this light, there is very much a question mark over the company’s future. As an additional factor, transparency is relatively limited, although to some extent this probably goes hand in hand with the nature of the company’s business.

Summary

The reversal of the interest rate trend has created positive momentum that CFT has been well able to exploit based on international expansion and efficient use of technology. Given this background, the acceleration of growth could continue and take both revenues and profits to a higher level. Shareholders will continue to be the beneficiaries of positive business development. As shareholders of CFT, Bottinelli and Lechthaler sum up their investment rationale as follows: “Unlike a big bank, CFT is an owner-managed company. Senior managers have the majority of their net worth bound up with the company, which protects minority shareholders from major risks. Overall, we believe the current market valuation gives the stock an attractive opportunity/risk profile. And the share buyback programme could give the stock an additional boost.”

The valuation is indeed attractive, with potential upside. The P/E ratio stands at 10x, the dividend yield is close to 5.0%. The P/B and P/S ratios likewise look fairly low at 2.0x and 0.9x respectively. Growth momentum is persisting, with revenues increasing by 8.1% in the first quarter of 2023. Although the risks to which the company is exposed – such as a change in management or shareholder base or a new cyclical phase of QE and low-interest policy – are not negligible, the opportunities for CFT stock appear to outweigh these.