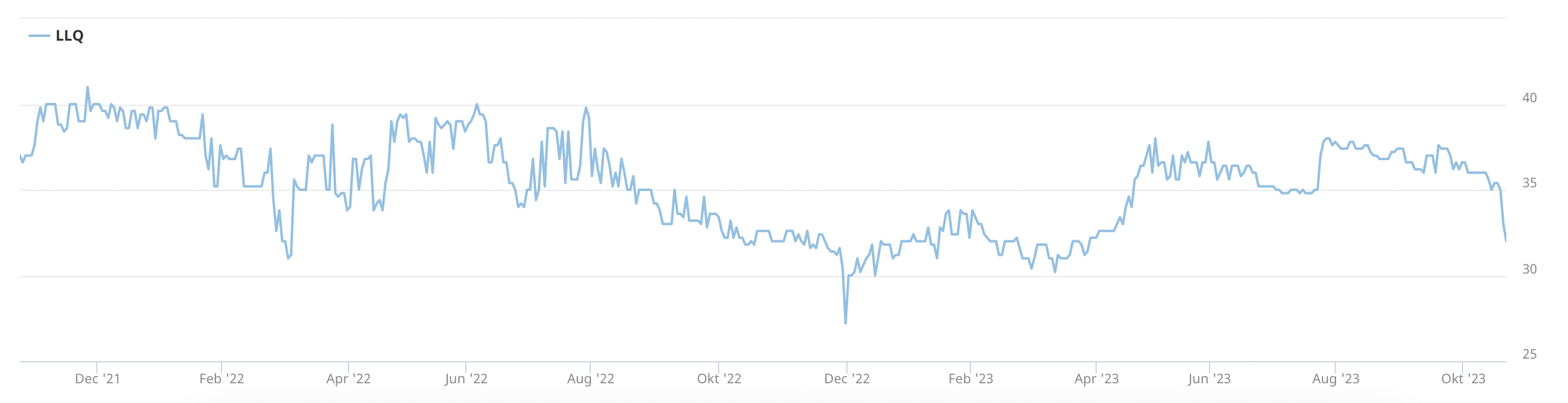

For many years, luxury goods stocks were in vogue on the stock market, although Lalique was only able to participate to a limited extent. However, the leading lights of the luxury universe such as Richemont and LVMH have seen their stock prices slump since the summer. Growth rates in the luxury goods business are tailing off. Even the share price of Lalique, which initially appeared to be resilient, has ceded ground recently.

Lalique stock started the year at CHF 32 and rose to a peak of CHF 38. After the latest period of price weakness, the stock is now back down at around CHF 33. Viewed over a one-year time horizon, the performance of Lalique stock has lagged well behind that of LVMH, with a price gain of 1.2% versus 4.3%. The correction of recent months notwithstanding, the relative performance of LVMH over a three-year period (53.4%) towers over that of Lalique (13.8%). While this comparison is only valid to a certain extent given their very different sizes, both companies have broadly diversified product categories in their portfolios, so the overarching demand trend in the luxury goods business feeds through in a similar way.

Sales rise – but not as sharply as costs

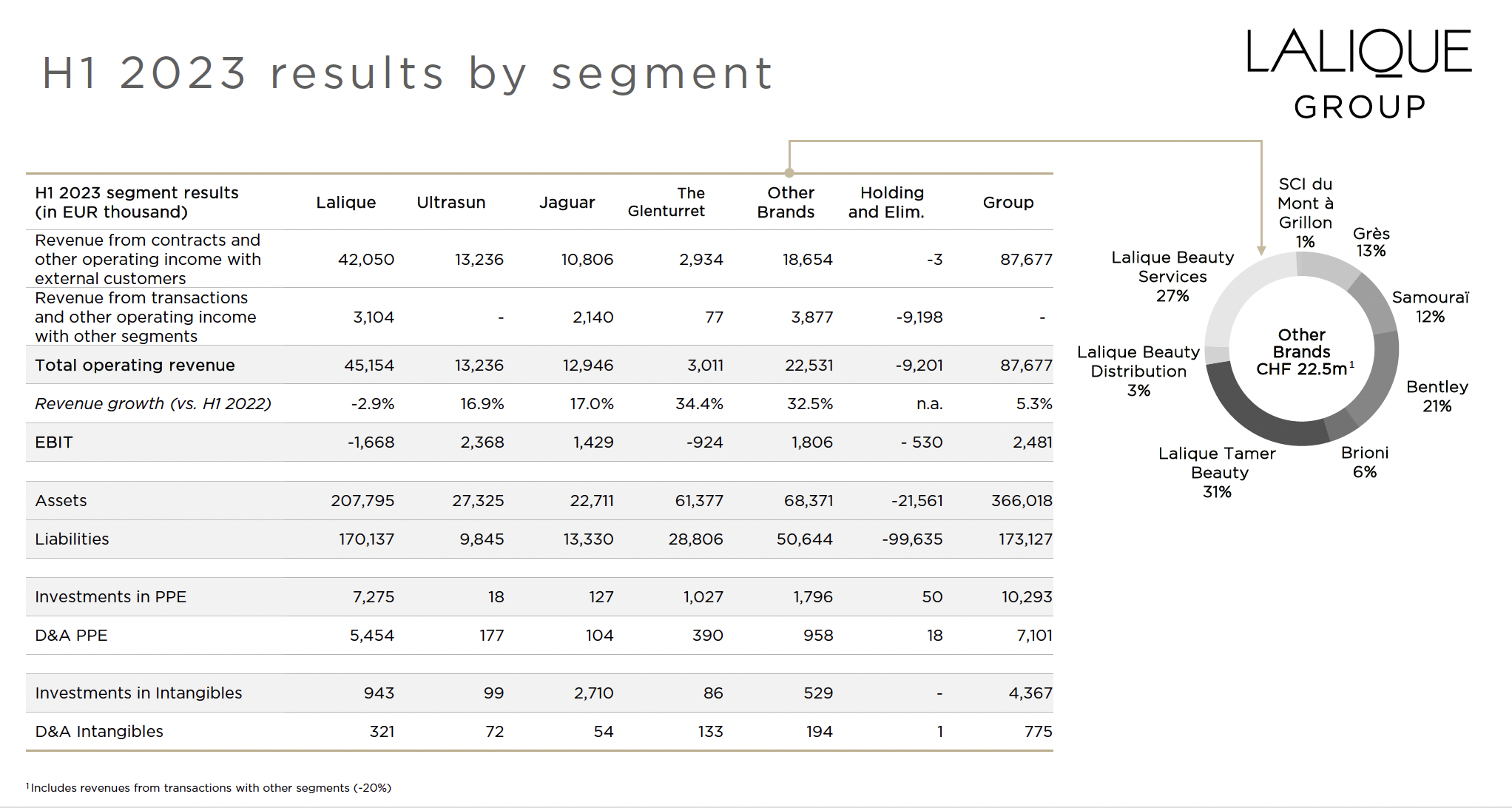

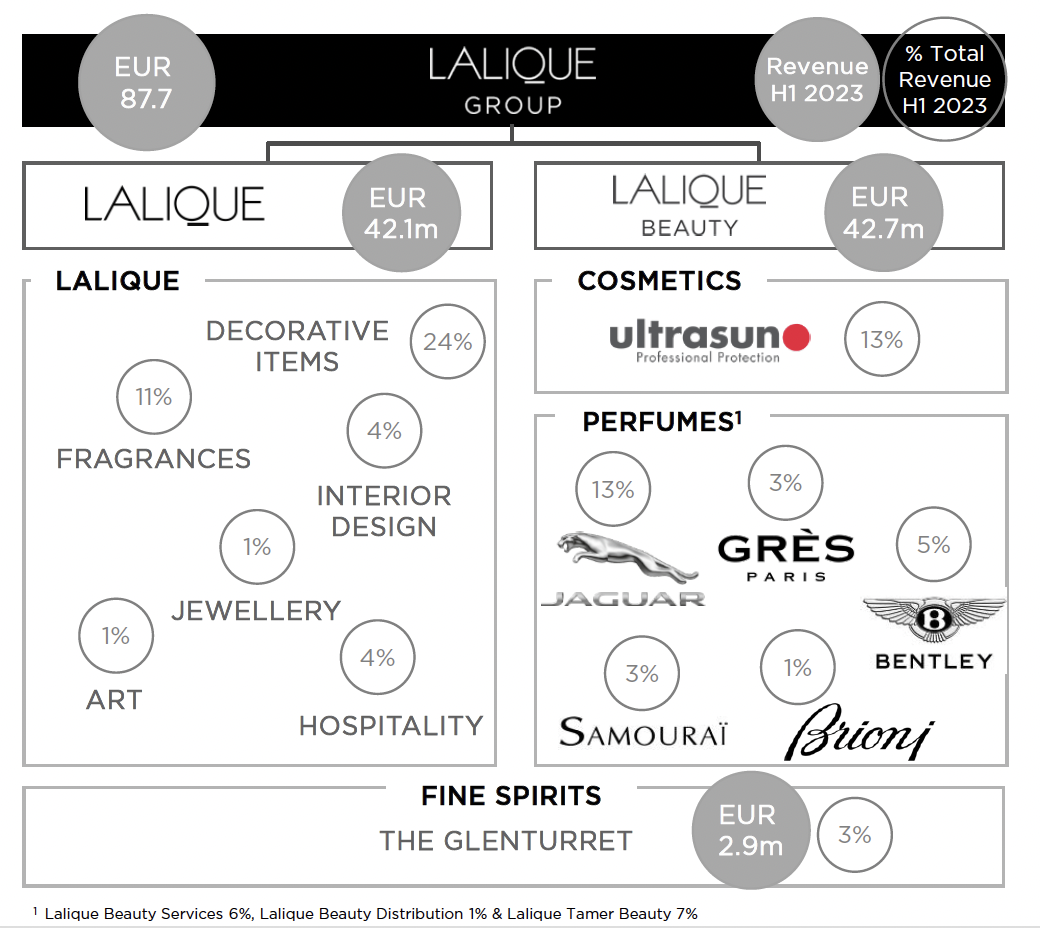

In the first half of 2023, Lalique’s sales rose by 5.3% to EUR 87.7 million. The growth rate in the prior-year period was as much as 28.5%, although the effects of the pandemic and other special factors played a role here. While the company’s international expansion and diversification of income streams are proceeding according to plan, they also incur costs. A good example is the company’s acquisition of Scottish whisky distillery The Glenturret. Sales rose by 34% to EUR 3 million in the first six months of the year, and Lalique is intent on increasing them further. This has inevitably had an impact on marketing costs. The Visitor Centre, Bar and Restaurant have been fitted out in a luxurious way, and their operation has necessitated an increase in headcount. In total, the sales contribution of this business to the Lalique Group amounts to 3%. And the quality of this operation does not appear to be in doubt: In the first half of 2023, The Glenturret Lalique Restaurant was judged to be the best restaurant in Scotland.

Perfume business of paramount importance

The perfume business is more important, accounting for 36% of the Group’s total revenues. Of this figure, 11% relates to the proprietary Lalique brand. 13% comes from the perfumes of the licensed Jaguar brand, 5% from Bentley, a further 3% each from Grès and Samourai, and 1% from Brioni. One attraction of the perfume business is the very high margins that can be achieved. The model of marketing perfumes created in-house under famous brand names has proven to be successful, even if the corresponding sales in the first quarter – such as CHF 13 million the case of Jaguar – do not sound that impressive. But in addition to high margins, of key importance here are the impressive growth rates of this business, which have gained momentum through joint ventures (e.g. with the Tamer Group in the Gulf region). In the first half of 2023, sales growth for Jaguar and Samourai revenues worked out at 17% in each case, while Grès recorded growth of 5%. By contrast, Bentley fragrances suffered a sales decline of 16% due to supply problems.

EBIT records sharp decline

EBIT declined at Group level, as well as in the perfume segment. The figure of EUR 2.5 million for the first half of 2023 compares with EUR 6.3 million in the prior-year period. Of this year’s figure, EUR 1.8 million related to the perfume segment. The EBIT margin at group level declined accordingly to 2.8%, while net profit amounted to EUR 0.6 million. This weak result is attributable to general cost increases, with material expenses – by far the largest cost block – rising by EUR 5.6 million to EUR 40.8 million. Personnel expenses rose by EUR 2.5 million to EUR 22 million, reflecting both new hires and wage increases. The high level of investment is also reflected in an EUR 0.5 million increase in depreciation, amortisation and adjustments to EUR 7.9 million. Earnings per share fell to just EUR 0.15, compared to EUR 0.74 for the first half of 2022.

Sun protection performing well

One highlight is the cosmetics segment containing the Ultrasun brand, which accounts for 13% of total revenues. Ultrasun sales increased by 16.9% to EUR 13.2 million. As marketing expenses were exceptionally high in the first half of 2022 and have now normalized, EBIT more than doubled here to EUR 2.4 million. The EBIT margin is likewise very impressive at 17.9%. So far, the premium provider Ultrasun has been mainly familiar in Switzerland, but the potential for growth in the sun protection business is ubiquitous. For example, sales in the UK rose by as much as 21% in the first half of 2023, while plans to tap into the Chinese market – after delays due to the rigorous Covid policy of the Chinese government – are now once again being pursued more vigorously. The aim here is for market launch to be supported by a Chinese distribution partner. The company has ambitious plans for expanding Ultrasun sales in the US too.

Higher energy and material expenses

While perfume and cosmetics, which together account for half of all Lalique sales, have proved to be resilient and profitable, the crystal manufacturing business was more severely hit by the increase in energy and material prices. This segment accounts for 24% of sales. Investment in expansion and renovation combined with technical problems affecting the new melting furnace saw sales largely maintained, but the segment’s EBIT moved into negative territory. In Zurich, the Lalique Flagship Store moved to a new location. Meanwhile, the company is planning to open two new stores in China.

Hotel business delivers 7% growth

The Lalique segment also includes the hospitality and interior design businesses, both of which contribute 4% to Group sales, while art and jewellery each contribute 1%. Performance in this area has been mixed. While hospitality generated sales growth of 7%, the perfumes of the proprietary Lalique brand experienced a decline of 3%. Overall, costs in this segment rose by 11%, which explains the EUR 5.5 million decline in EBIT to EUR -1.7 million.

Expansion and inflation

The development of EBIT looks unsatisfactory at first glance. If the half-year EPS figure of EUR 0.15 is extrapolated to the year as a whole, the resulting P/E ratio works out at over 100x. However, closer scrutiny of the different segments and brands reveals more dynamic underlying operating developments. One factor that was not wholly foreseeable was the magnitude of inflation in the first half of the year, particularly for materials and energy. By contrast, other expense items – such as the 13% rise in personnel expenses to EUR 22 million – were only to be expected given the rise in headcount in connection with the company’s expansion plans and significant investment in certain areas, such as The Glenturret complex and the new melting furnace in the crystal segment.

Majority of segments enjoying strong growth

When viewed on the basis of growth rates and EBIT, the picture looks promising and points to a significant improvement in profitability going forward. A half of all revenues is generated by the Ultrasun, Jaguar and other perfume segments. When combined, these segments delivered EBIT of EUR 5.6 million in the first half of the year. Margins are high, despite new launches and the associated marketing expense. The growth rates range from 17% for Ultrasun and Jaguar to as much as 32.5% for the other perfume brands.

Positive outlook for whisky

The Glenturret and Lalique segments both posted negative EBIT margins in the first half of 2023. However, the former recorded sales growth of 34.4%, which had the effect of improving EBIT to EUR -0.9 million. The losses are attributable to the takeover and relaunch, the realization of a hotel and restaurant, and investment in expansion – including in climate-compliant processes such as the electrification of the machine pool. The company is striving for break-even here in the second half of 2023, so the segment should make a positive contribution to EBIT in 2024.

Villa Florhof set to open in 2024

All sorts of activities are subsumed under the Lalique segment. The EBIT margin here, which stood at 8.3% in the first half of 2022, has slumped to -3.7%. This is in part due to higher energy, material and personnel expenses, but also to the expansion of the hotel and restaurant business. Lalique now operates three hotels, and considerable investment is currently being channelled into the renovation and refit of the highly traditional Villa Florhof hotel in Zurich, which is set to open in 2024. The high level of investment overall is clearly apparent in the company’s balance sheet: Intangible assets and plant and equipment have recorded a year-on-year rise of EUR 6.5 million.

Diversification a strength

The company has made it clear that it will continue to pursue its diversification strategy. In an environment characterized by ongoing uncertainties, the broad spectrum of activities should be viewed as a positive. Specifically, the launch of further perfumes is planned, including the first Lalique fragrance for men. Sales should be buoyed by new distribution partners and contracts in the Middle East, Asia and Latin America. The same is also true of the internationalization of the Ultrasun sun protection brand. Furthermore, the market launch of a first gin brand is planned. Capacity is being increased both in crystal manufacturing and at The Glenturret, while at the same time the company is seeking to decarbonize production processes to the greatest extent possible, be it through the use of waste heat or electrification. Sustainable business is high on Lalique’s agenda, and the company’s objectives, measures and progress in this area are disclosed in the Sustainability Report on an annual basis.

Outlook

A further plan for 2024 is the relaunch of the Fabric Frontline silk label. Likewise in the pre-launch phase is the new perfume range under the global Superdry fashion brand. Improvements on the cost front can be expected thanks to forward contracts for energy in 2024 and 2025. For the second half of 2023, management is expecting an improvement in the EBIT margin along with sales growth “in the high-single-digit percentage range”. Over a medium-term horizon, growth in the mid-single-digit percentage range is being targeted, along with an EBIT margin of 9-11%. The expectations of investors are therefore being kept in check. Bearing this in mind, it is quite possible that the company could surprise them on the positive side.