Image source: vzug.com

Metall Zug’s decision to spin off V-Zug Group almost three years ago was a bold one. The primary markets were ice cold, and coronavirus was crippling public life. Against this backdrop, the stock market welcome was initially cool – the price fell by 15% in the first five months. But the investment community then «discovered» this strong-brand stock, triggering a rise that would amount to 150% by August 2021. The market’s mood has long since flipped back again. The three years of the coronavirus and Ukraine crises have also inflicted their fair share of damage on V-Zug, as is clear from the 2022 financial statements. Yet the moderate price level now makes the stock look attractive once again, as the international business is growing powerfully.

In the area of household devices, V-Zug is the clear market leader in Switzerland. According to the most recent survey, 61% of all Swiss would buy a V-Zug device. Although the company’s high market penetration is proof of its success, it also means that significantly increasing market share in the domestic market is unrealistic. The picture looks very different in the big wide world outside of Switzerland. Indeed, the potential here for market penetration by the international innovation leader V-Zug looks to have almost no limits.

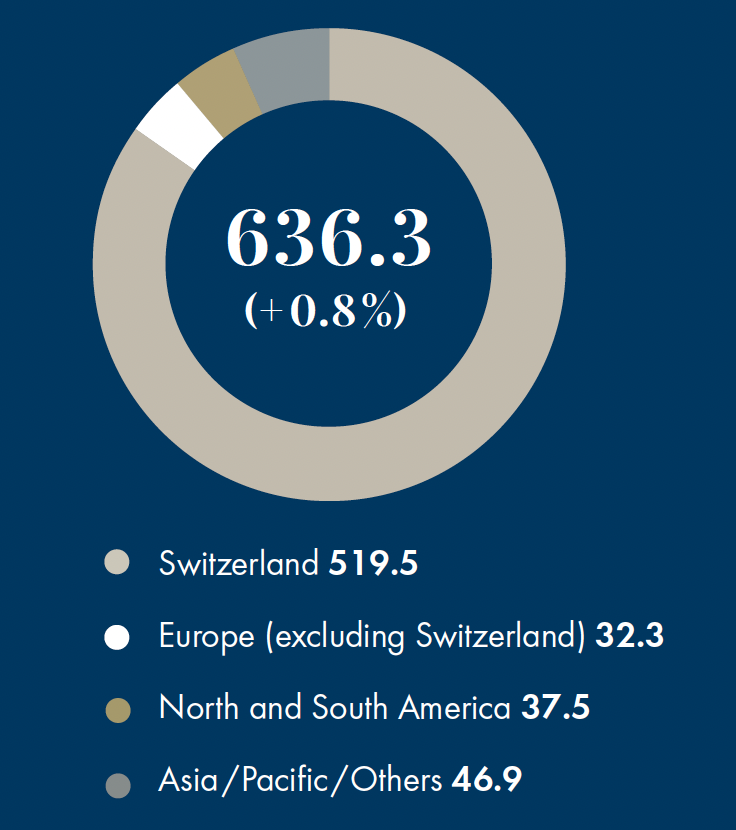

Group revenues stagnate

In 2022, the net sales of the V-Zug Group edged up by just 0.8% to CHF 636.3 million. But whereas net sales in Switzerland declined by 3% to CHF 519.5 million, growth in other regions amounted to a handsome 18.4% – and as much as 21.8% in local currencies. Sales outside Switzerland rose to CHF 111.7 million. Of this figure, CHF 32.3 million relates to Europe, CHF 37.5 million to the Americas, and CHF 46.9 million to Asia-Pacific and other markets. While in Switzerland the pandemic-related «home nesting» mini-boom subsided in 2022, international growth has been accelerating in recent years – from 11.3% in 2019 to a current level of 18.4%.

Internationalization as priority

International expansion was a stated target even before the spin-off in 2020, and as the figures show, V-Zug has been consistently successful in delivering in this area. Given the low initial base, the growth figures might look more impressive than they actually are, but they leave little room for doubt that the company’s growth potential lies primarily in markets outside of Switzerland.

Innovation leadership

Even when viewed dispassionately, the company ticks the key boxes in this respect. V-Zug has been the undisputed market leader for household devices of all types in the sophisticated Swiss market since the 1950s. The company’s innovative spirit dates back to 1949 and the market launch of the «Tempo» – the first small washing machine in Switzerland. This was the start of a run of successes that continues to this day. The company would go on to offer Swiss consumers automatic washing machines, dryers, dishwashers, and in the last 20 years increasingly also fridges and new cooking technologies such as induction hobs, steamers, and vacuum cooking solutions.

Differentiating features

From the very start, all the company’s devices and concepts have been characterized by quality, longevity, reliability, and sustainability. Indeed V-Zug is essentially synonymous with energy efficiency in the area of household devices. Moreover, buyers of its products can rely on a rapid, first-rate service team that resolves problems and provides the appropriate replacement parts even for older models. Product design is also emphatically high-end, echoing the intrinsic quality of the devices. At the end of their life cycles, up to 80% of products are recycled – a figure the company is looking to increase further. Moreover, V-Zug also intends to facilitate the reuse of old but functioning devices in a second-hand market when customers order a replacement. In terms of Scope 1+2 emissions, V-Zug has been operating climate-neutrally since 2020. To compensate for its emissions, which were reduced by a further 14.9% in 2022, the company has been financing a reforestation project in Scotland since 2020.

EBIT margin slumps to 1.6%

Sales stagnated in 2022 due to the high proportion accounted for by the domestic market. This development had already been looming on the horizon. Although consumer demand remained at the high level of the previous two years, production was held back by component supply issues. More worrying, however, were the rising costs of materials and freight. The unexpected severity of these cost increases last year resulted in the company’s margins being severely squeezed. EBIT fell from CHF 62.7 million in 2021 to just CHF 10.3 million in 2022, and the EBIT margin slumped accordingly from 9.9% to just 1.6%. Price increases are passed on in staggered fashion, with a time lag, and following consultation with the relevant stakeholders.

Earnings contraction and dividend policy

The Group net result slumped by 85.7% to CHF 7.9 million, equivalent to a net profit margin of 1.2%. The key driver of this development was a 12.2% rise in the cost of materials. Elsewhere the company exercised cost discipline in 2022. By contrast, income tax declined by CHF 4.5 million to CHF 2.1 million. Earnings per share therefore came in at CHF 1.23 for 2022, well below the figure of CHF 8.62 for the previous year. No dividend will be proposed, in keeping with the company’s policy: At the time of the spin-off it was made clear that no payout would be envisaged for the independent V-Zug for three years due to the high level of investment already made, as well as the ambitious investment planned for the future. In 2022 too, capital expenditure (in both tangible and intangible assets) amounted to an impressive CHF 50.2 million. Going forward, i.e. in all probability from 2024 onwards, the company’s policy will be to distribute between 20% and 40% of annual profit to shareholders.

Correlation with peer group

At the current price level of around CHF 80, the market capitalization of V-Zug stands at just over CHF 500 million. This is slightly less than equity capital, and 20% below the level of sales. However, a comparison with peers Electrolux and Whirlpool quickly shows that these larger and more internationalized competitors did not fare any better in the face of last year’s crisis. The stock of Electrolux currently languishes some 60% below its high recorded in the summer of 2021, whereas that of Whirlpool has halved over the same timeframe. Indeed, Whirlpool actually recorded a loss of USD 1.5 billion for 2022, with a slightly reduced sales level of USD 19.7 billion. Viewed over the longer term, both stocks exhibit an extremely cyclical pattern, marked by alternate price slumps and rapid recoveries.

Sights set on premium segment

In contrast to competitors Whirlpool and Electrolux, which in many respects are very comparable, V-Zug does not pursue a multibrand strategy, nor does it have any desire to cover all price segments. V-Zug is unashamedly a premium provider. What’s more, the company has not been active in international markets as long as these larger players, and can therefore take a targeted approach to expansion. The Zugorama concept is a tried-and-tested way of breaking into selected countries. The Zugorama showrooms in Zug and Chur were redesigned in 2022, while new studios were opened in Paris and London. For 2023, the company’s «Metropolitan Strategy» envisages a relocation in Singapore to a better location and accelerated first-time openings of Zugorama showrooms in Vienna, Berlin, Hamburg, Milan, and Sydney. V-Zug also has a presence in China, Thailand, and Vietnam (among others) through distribution companies. The momentum of internationalization can therefore be expected to pick up over the next few years.

Vertical factory

With the exception of a factory to manufacture special components in China, all production takes place in Switzerland. Headcount currently stands at 2,200 employees in total. In order to turn the relatively higher costs of production in a high-wage country into a competitive advantage, previous majority shareholder Metall Zug had invested substantially in a vertical factory at the company site in Zug even before the spin-off. Moreover, as part of the spin-off V-Zug was supplied with liquidity amounting to CHF 110 million to press ahead with its transformation in the Zug technology cluster. Metall Zug remains a significant shareholder in V-Zug with a stake of 30%.

Fit for the future – thanks to strong investment

In the three years since the spin-off, the investment drive has continued: New buildings owned by V-Zug are attracting tenants and enjoying rising rental income. As well as being confirmation of the company’s commitment to Switzerland as an industrial centre, the expansion of production should also be able to satisfy future demand in a profitable way. The exceptionally efficient production process in the Industry 4.0 factory is truly pioneering, including with a view to future-oriented, climate-neutral energy supply. The factory even has a net positive climate footprint, as it combines different energy sources such as solar, waste heat utilization, hydrogen production, and groundwater heat.

«Sustainability in the DNA»

This is also a reflection of the company’s commitment to sustainable business. «Sustainability is in our DNA» reads a headline in this year’s letter to shareholders. And unlike at many companies, this is nothing new. Including the period when it was owned by Metall-Zug, V-Zug has been producing and publishing a Sustainability Report for more than a decade now. With effect from next year, V-Zug will transition to integrated reporting, merging its Annual Report with the Sustainability Report. The focus of 2022 was on the establishment of the circular economy and cooperation with recycling companies.

Market opportunities

V-Zug is exploiting the opportunities presented by structural change. As a renowned manufacturer of premium devices and holistic concepts, this innovation leader remains a coveted partner even in the saturated Swiss market. For example, V-Zug is increasingly fitting out entire buildings with highly efficient and interconnected household technology, which has the effect of increasing the value of the customer’s property. A new concept that will allow the company to tap into the institutional market is «product-as-a-service». A key factor here is the ever more rigorous regulatory requirements that V-Zug already meets thanks to its sustainable business policy – unlike many providers that have long since outsourced production to low-wage countries. In Switzerland too, the company can exploit growth potential not just through its competitive edge, but also with its innovative concepts and products.

Outlook

The problem of supply bottlenecks began to ease in the second half of 2022. With the ongoing normalization of supply chains, catch-up effects in 2023 could once again lead to a positive growth rate in Switzerland. Together with the price increases scheduled to take effect over the course of 2023, this points to a normalization of the domestic market, which should therefore deliver growth in low single-digit percentage territory. By contrast, the stimuli for higher growth rates at group level will come from global expansion. The company has already set a clear course towards international growth, backed by the further development of both the product portfolio and the brand strategy. Digitalization and sustainability are characteristics that clearly differentiate V-Zug from the majority of its competitors. So far, the company has also done an impressive job of delivering on its brand promise in the Americas, Asia, and Australia. «Made in Switzerland» goes down well.

Summary

Supply problems, combined with rising prices for both materials and freight, took their toll on V-Zug in 2022. Earnings slumped dramatically. But the underlying growth dynamism remains intact. The country’s entry into numerous international markets has been well thought through strategically, with the aim of a high-end market positioning. This has gone hand in hand with substantial investment in production capacity in Switzerland. It is difficult not to be impressed by the efficiency of the vertical factory in Zug. Given the quality of products, their energy efficiency, the enduring popularity of Swiss design, and the digitalization and sustainability of both products and the production process, the drive to achieve high-end market penetration appears likely to succeed. Following the cyclical halving in price, the stock now looks cheaply valued. The likely return to an EBIT margin in the region of 8% to 10% would push the P/E ratio below 10x.