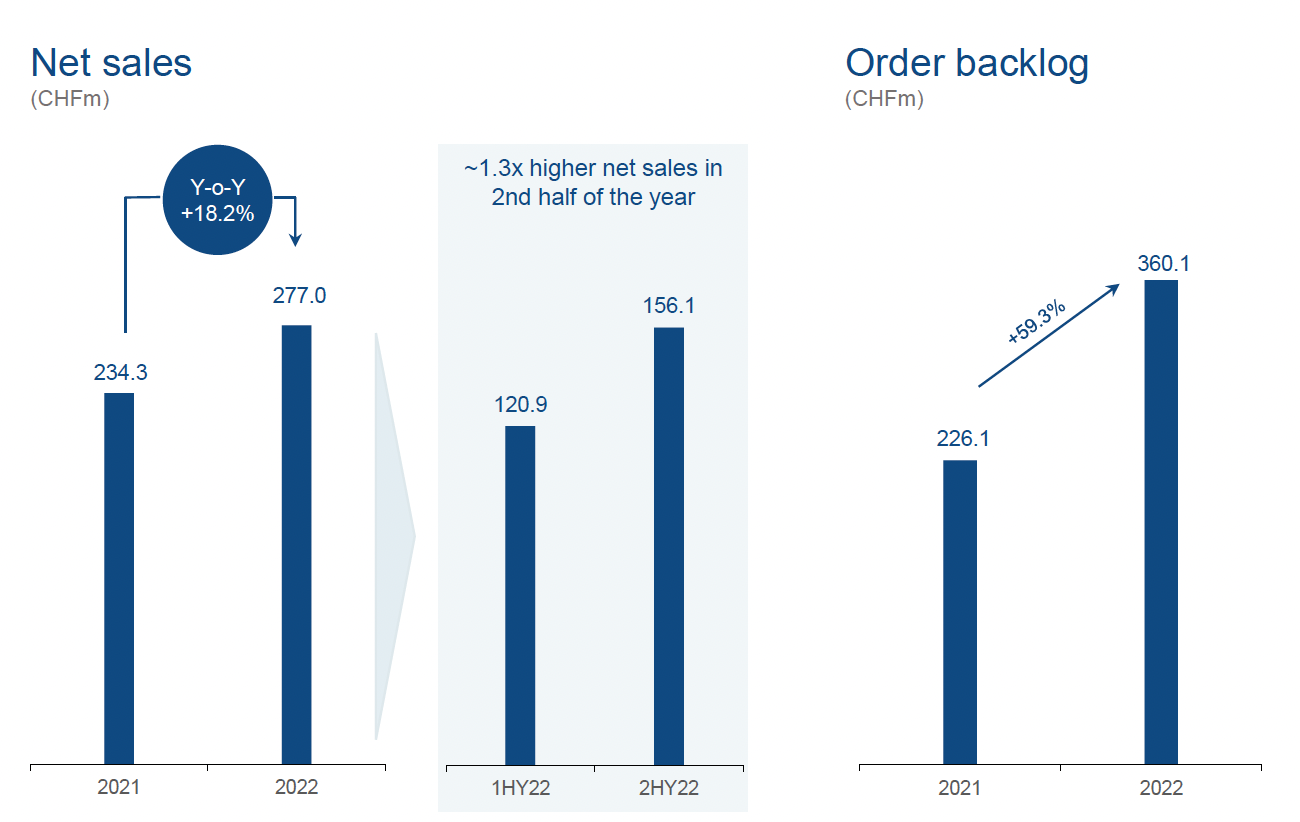

From an investor’s perspective, these few words sum up the first progress report on the performance of SKAN Group since its stock market debut in October 2021. Despite all the headwinds, the 2022 financial year proved quite something: Net sales rose by 18.2%, order intake by 46.9%, and the stock price has rocketed by 30% since mid-March.

Even at the time of the IPO, right in the middle of the pandemic, it was clear that SKAN would be quite an asset to SIX Swiss Exchange. The equity story accompanying the flotation was both insightful and concise, as set out in the accompanying analysis of schweizeraktien.net. And as is clear after the company’s first full year as a listed entity, SKAN is also now delivering the growth that was dangled as a prospect in the run-up to the flotation.

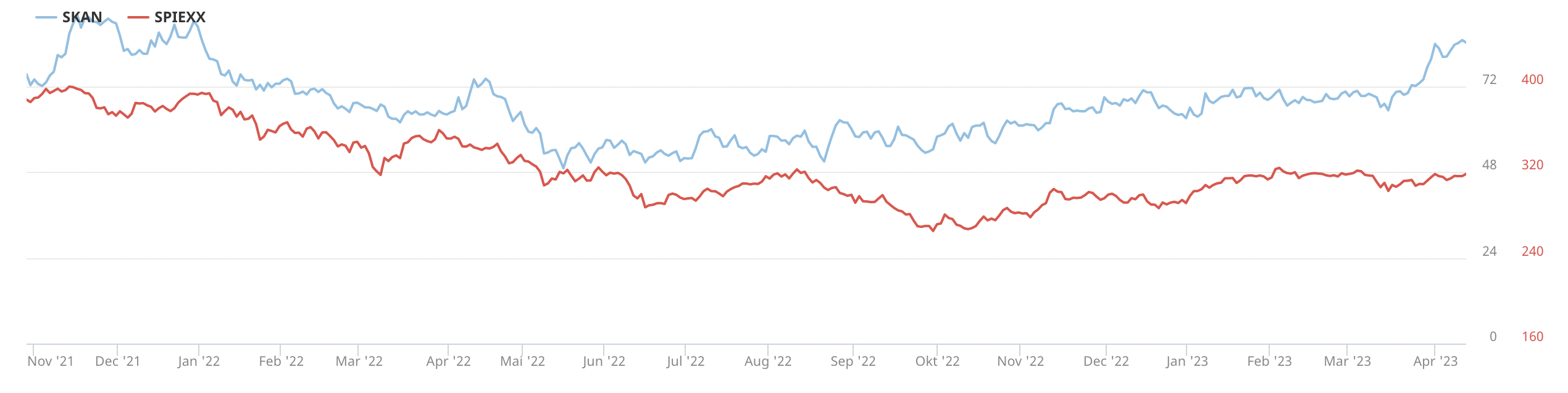

Relative strength

The IPO closed with the stock priced at CHF 54, which was at the upper end of the bookbuilding bandwidth. In the early days of secondary market trading the price surged briefly above CHF 90, but the stock then embarked on a downward slide until a nadir of CHF 49 was reached in June 2022. An ensuing trend reversal then saw the stock pick up strongly before closing the year at CHF 63. By contrast, Switzerland’s SPIEXX Small and Mid Cap Index did not hit its annual low until the end of September. In other words, SKAN’s stock’s relative strength in the difficult second half of 2022 was already a clear pointer to the outperformance that would follow in 2023.

Structural growth surge

Detail on the company’s products – isolators – and business model can be obtained by clicking on the above links to the IPO study. The pandemic and the unprecedented speed with which highly effective Covid vaccines had to be (and indeed were) developed, produced, and administered sparked off an accelerated boom for SKAN, the global market leader for isolators for the aseptic or aseptic-toxic filling of biopharmaceutical substances and vaccines. However, this boom should not be viewed as fleeting and/or limited to the Covid-specific situation, but rather as the manifestation of strong structural growth. In January 2022, CEO Thomas Huber responded to various questions in an interview for schweizeraktien.net.

Personalized medicine as growth driver

The challenges of the Covid era from 2020 onwards essentially lit the touchpaper for the upward surge of an existing trend at a higher level. A crucial factor here was the proof of concept and rapid breakthrough of mRNA technology. Many of the most recent drugs to come onto the market have to be injected. An absolutely critical aspect here is secure and contamination-free production and filling.

Isolators for the life sciences industry

Be it big pharma, biotech, or science and research – conventional, expensive cleanroom technology is increasingly being ousted by the more efficient and more cost-effective solution of isolators. The energy requirement of these devices is just 5% to 10% of that of established cleanroom technology. Moreover, injectable substances from the world of personalized medicine are firmly on the rise. Isolators have made huge progress in evolving from a specialized niche product to a widely used form of technology in the world of life sciences. Almost all the top pharma and big biotech companies are SKAN customers.

Forecasts met

As communicated during the IPO, 2021 sales were in line with forecasts, coming in at CHF 234.3 million. Both production and service capacities were increased as planned. The tempo of growth therefore increased to 18.2% in 2022 – once again in keeping with forecasts (which were for the “upper teens”). Sales rose to CHF 277 million. Working through the higher order backlog had already proved a challenge the previous year, and this “healthy problem” became even more pronounced in 2022: SKAN’s order intake increased by 46.9% to CHF 411.7 million, pushing the order backlog up by a hefty 59.3% to CHF 360.1 million. This gives the company considerable planning security for the next two years.

EBITDA margin rises to 14.5%

The development of operating profit has kept pace with advances on the sales side: EBITDA increased by 30.9% in 2022 to CHF 40.2 million, with the EBITDA margin improving by 1.4 percentage points to 14.5%. Although SKAN too was affected by supply chain bottlenecks and higher costs – above all for materials – the company ramped up its inventories at an early stage and thus managed to avoid disruptions to supply.

Income statement

Investments amounted to CHF 76.4 million, of which CHF 28.9 million was allocated to the expansion of the Görlitz production site in Germany. In addition, the strategically important stake in the Belgian company Aseptic Technologies was increased from 60% to 80%. Headcount rose by 165 in 2022 to 1,172 employees, not least to keep step with the company’s strong growth. Personnel costs are the company’s largest single cost block and rose from CHF 107.7 million to CHF 124.9 million. That said, as a proportion of sales they declined slightly to 45.1%. Materials and external services amounted to CHF 76.5 million last year, with the proportion of sales barely changed at 27.6%. However, at CHF 21.4 million, net profit was only slightly higher than the prior-year figure. Earnings per share came in at CHF 0.84, unchanged from last year. The dividend is being raised by 1 centime to CHF 0.25 per share. The company’s dividend policy envisages the distribution of 30% of reported annual profit.

Above-average growth rates

The SKAN Group impresses from a relative perspective too. According to market studies carried out by L.E.K., the increase in SKAN’s order intake in 2022 was four times greater than the isolator market segment overall. This is reflected in a strong book-to-bill ratio of 1.5, which bolsters the positive outlook.

Business model

SKAN’s business is divided into two segments. Equipment & Solutions manufactures systems and components, and at CHF 207.7 million accounts for the largest share of sales. The EBITDA margin here amounted to 11.1% last year. By contrast, the EBITDA margin of the Services and Consumables sector is much higher and came in at 24.8%. The striking aspect of the business model is that the sales base of the Services & Consumables segment grows with every system installed or retrofitted by the company. Further stimuli come from the renovation of old cleanroom technology, an area in which renewal is typically required after 20 years at the latest. SKAN sees considerable potential in the retrofit business.

Injectables on cusp of exponential growth

But the real driver of demand is the growing proportion of new biopharmaceutical substances appearing on the market that must be administered through injections, which in the case of genetic and cell therapies lies at 75%. Although this is not something particularly evident or visible in the market at the moment, SKAN’s pipeline gives an insight into the significant developments that are currently at the preparatory stage and therefore yet to come to fruition. In the 2022 Annual Report SKAN outlines its involvement in more than 80 projects with a variety of partners. The development pipeline of Aseptic Technologies for closed vial filling rose by 30% in 2022 to some 400 substances. And to date, only three drugs have reached the stage of receiving approval from the relevant authorities for commercial production – the third one just recently.

Paradigm shift

It does not take a great leap of imagination to appreciate the impending exponential development that awaits SKAN, with the prospect of eye-popping growth rates. Quite simply, a paradigm shift is taking place in medicine, away from the established chemo-pharmaceutical therapies that effectively “use a sledgehammer to crack a nut” in favour of individualized, patient-specific therapies with fewer side effects. A key difference worthy of note here is that the new personalized medications take liquid form and are heat-sensitive, which means conventional heat-based sterilization is not an option. The solution to this problem lies in aseptic or aseptic-toxic production and filling in closed vials – which is precisely what SKAN does.

Rising market share

Additionally worthy of mention here are a couple of further developments that will work to SKAN Group’s advantage. In the 2022 financial year the company was able to further expand its leading position in the isolator market. Even at the time of the IPO its global market share stood at 25% – and as much as 35% in the high-end segment. Higher market shares through innovation surges also provide the best platform for price leadership.

AI as cost-cutting tool

The second development is the increased application of AI. Prior to the IPO, as much as 30% of personnel costs related to fulfilment of documentation obligations, which are now increasingly being handled by intelligent robots. No doubt the competition is pursuing this route too, but SKAN is likely to be a step ahead, as the relevant approval authority in the US (the FDA) was pointing to SKAN’s “good manufacturing practices” even before the IPO. This can be expected to gradually reduce the company’s cost base. A further sales argument is the use of AI in the maintenance and optimization of systems installed with customers. An absence of disruptions means no sales outages for customers and therefore planning security. This is an area in which the comprehensive service offerings of SKAN – which guarantee the flawless functioning of isolators and the filling process under all sorts of conditions – have an edge.

Outlook

Due to the high order backlog and the unrelentingly high order intake, SKAN’s business remains on a dynamic trajectory. The scaling of production does represent a challenge. As things stand, the company has production sites not just in Switzerland and Germany, but also in Belgium, Japan, and the US. The company has started the year well and expects sales growth in the “upper teens” area for the year as a whole, with the EBITDA margin expected to come in at around 13-15%. This is also aligned with the company’s medium-term planning, which envisages EBITDA getting closer to the 20% mark.

ESG conformity

Product, people, planet – such, in a nutshell, is how SKAN sums up its priorities. The predominant product used in isolators is high-grade steel, which is fully recycled. Processes are being simplified by ongoing digitalization, and business flights are becoming less frequent. A “no plastic” initiative has been launched in the company’s offices. Buildings are fitted with photovoltaic systems to reduce energy consumption, and the vehicle fleet of service personnel is being converted to e-mobility. A key area of focus for SKAN is its workforce. The development of talented staff is encouraged, and the input of employees is valued, not least because this contributes significantly to the company’s success. Detailed sustainability reporting is aligned with GRI standards.

Summary

SKAN Group has surprised investors on the positive side, with strong figures that have exceeded expectations and testify to the rude health of the company’s business. Indeed, the biggest challenge confronting management at the moment is to manage the growth and scaling of global business development in an optimum way. So far it has delivered on this objective convincingly, and there is nothing to suggest any change to the strong growth trend. Companies with an outstanding position in a rapidly growing market also justify higher valuations, particularly when they happen to be market and technology leaders. On a more cautionary note, SKAN stock is currently trading at a P/E of 100x, which means a fair amount of future profitable growth has already been factored into the price.