Solar power is «in»! The only pure solar energy play on SIX is Edisun Power. The stock has been traded since 2008, at which point it was the one of the few listed solar power companies still trading in Europe. And although Edisun shares rose steeply in the five years up to 2019, they have predominantly trended sideways since then. In 2022 the company announced an opportunistic change in strategy, which should give a further boost to earnings development.

Markets change, and the basic rules of economics apply in the world of solar energy too. To start with solar cells were expensive and could not compete with cheap fossil fuels. This delayed the widespread adoption of this climate-neutral form of energy for a long time. Edisun Power is a pioneer in this field. It was founded back in 1997 and put its first photovoltaic (PV) facility into operation in Zurich in 2002.

The appeal of solar

In the meantime, the production costs of solar energy have long since fallen well below the level of so-called «grid parity», as the mass production of solar modules and their enhanced efficiency have drastically reduced the price of both procurement and operationalization. Even before the surge in energy prices following Russia’s invasion of Ukraine, production costs had fallen well below the prevailing costs of fossil fuels. The profitability of green energy producers has therefore risen sharply in recent times. What’s more, further declines in production costs are contrasting with higher energy prices. Margins are generally increasing.

Figures for H1 2022

In the first half of 2022, the sales of Edisun Power rose by 8% to CHF 9.2 million when expressed in the company’s reference currency, but by as much as 14.7% in local currencies. The EBITDA margin rose to 76%, and net profit surged by 148% to CHF 6.2 million. However, the majority of solar power produced is fed into the electricity grids of the corresponding countries at fixed rates of compensation. As well as Switzerland and Germany, the portfolio includes installations in Portugal, Spain, France, and Italy. Contract terms are typically set for a period of 5 to 10 years, but in some cases may extend to as much as 25 years. The way contracts are structured differs from country to country, as well as from project to project. But essentially this setup gives Edisun Power predictable income streams with high EBITDA, and this in turn allows it to pursue the acquisition, financing, and implementation of further projects. The number of solar power plants has risen continuously, and now stands at 39. However, the latest acquisition in Portugal has broken the mould – for the first time, the electricity generated will be systematically sold at spot prices, with guaranteed feed-in rates of compensation being eschewed altogether. This is in keeping with the current trend in the industry of significantly increasing the proportion of spot sales in order to benefit from much higher prices than those that applied in previous years.

Project portfolio

Edisun Power has worked closely with its partner Smartenergy AG (another Swiss company) ever since 2017, and now pursues a scaling strategy. Although only 107 MW of capacity is currently installed, as at the end of June 2022 Edisun Power had a project portfolio volume of 940 MW. A transaction completed in 2019 with a project volume of CHF 162 million – which accounts for the lion’s share of the portfolio, as it encompasses 17 projects and 703 MW – led not only to the release of capital to the partner Smartenergy through bond issues and capital increases, but also to a gradual and substantial increase in that company’s stake in Edisun Power itself, which now stands at 33.1%. The structure of the transaction raises all sorts of questions from a governance perspective, but it should at least be pointed out that the corresponding resolution was passed solely by the three independent members of the Board of Directors.

Lean and efficient organizational structure

Edisun Power is a very lean company that requires little in the way of personnel, including at managerial level. Following the departure of the CEO in 2021, no replacement was appointed. Management of the company is now the responsibility of the Delegate of the Board of Directors, Horst Mahmoudi. The decision to operate without a CEO should not be viewed as definitive. It is rather a case of the Board of Directors wanting to implement the change of strategy announced in the first half of 2022 directly and without any delay. However, Mahmoudi is also the sole proprietor of Smartenergy, a much larger company with a workforce of 150. Both companies cooperate by sharing tasks, and clearly create value by operating in tandem.

Original business model

The business model pursued by the company since it was founded has been to project, finance, and install solar facilities – and then maintain them. So far, 39 PV facilities have been built up in six countries. Growth has been financed by a combination of capital increases and bond issues, as well as through retained earnings. Showing considerable foresight, the company has also acquired a truly impressive portfolio of projects with a volume of 940 MW. The lion’s share of this portfolio was obtained before the surge in energy prices, i.e. before the war in Ukraine left Western Europe’s energy supply significantly exposed to Putin’s all-out pursuit of asymmetric warfare.

Change of era for solar energy

This change of era has led to a higher appreciation of the value of «energy autarky» right across Europe. Renewable energies, which are produced and consumed regionally, are now very much at the top of government priority lists. Within a short space of time, the EU has increased the target for renewable energies in its energy mix by 2030 in two steps, from an original level of 32% up to the current level of 45%. The failures of the past are now putting pressure on the political establishment to act. One of the consequences of this development is that energy projects can be sold to financial protagonists at handsome prices. This situation is not dissimilar to the scenario of a cheaply acquired land bank which – as the result of a huge surge in demand – can be opportunistically monetized in part now, rather than developed in full over the next 10 or 20 years.

New strategy

This is the core of the company’s strategy change. Edisun Power expressed this in figures in its half-year report as per the end of June 2022: The company is seeking to expand its own power plant park to 300–350 MW, while at the same time selling 600 to 700 MW of its project portfolio to green infrastructure funds, utilities, pension funds, and large corporates. The existing buy-and-hold strategy is therefore being expanded to include a partial, essentially opportunistic buy-and-sell strategy.

New financial targets

Edisun Power is sticking to its target of achieving an annual sales growth rate of 20% by 2025. Other targets including keeping the EBITDA margin above 70%, with an equity ratio of at least 40%. What’s more, the company intends to increase its dividend on an ongoing basis. This is a strong signal, as the dividend has remained at an unchanged CHF 1.10 per share for the last three years. This announcement also testifies to the company’s confidence that its strategy change will allow it to deliver better earnings in the current environment, which looks to have undergone a permanent structural change. This in turn should be well received by the capital market.

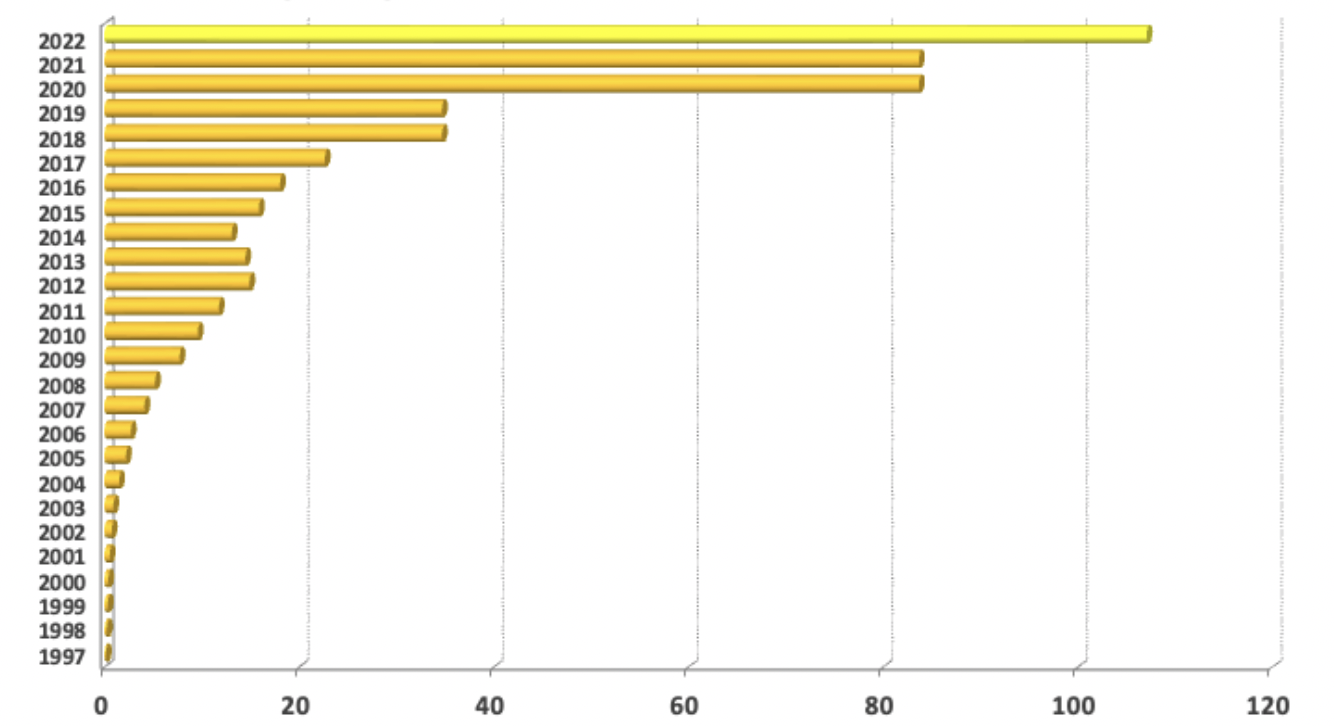

The 2017–2021 era

Over the last five full financial years, earnings per share have developed erratically, as have EBITDA and EBIT. This is partly attributable to the company’s intense investment activity, but also reflects the character of the projects implemented by the company, which only generate earnings after completion and the ensuing commencement of feed-in activity. Last but not least, the varying intensity of sunshine plays a role too.

Turning point in first half of 2022

The first half of 2022 marks a trend reversal in the figures reported by the company. At CHF 5.98, earnings per share outstripped the figures reported in the record years of 2018 and 2019, namely CHF 5.93 and CHF 5.96 respectively. And ever since the half-year report was published in August, it has become clear that earnings per share would also hit record levels for the 2022 financial year as a whole. Whether this turns out to be CHF 8, 10 or even 12 can hardly be predicted given the paucity of available information. Apart from anything else, no ad-hoc press releases have been issued in respect of substantial project sales, even though the sale of 185 MW of project volume was planned in the second semester of 2022. Other recent transactions, especially in Spain, were executed at very attractive prices.

Quite how the company’s profit figures will be impacted by the most recent operationalization of a 23.4 MW solar park in Portugal, which commenced activities in November 2022, remains to be seen. In this case, the solar electricity generated will be sold at spot prices for the first time in the company’s history. Production at this site accounts for around a fifth of all company capacity, and should therefore be of crucial importance to the profit contribution. When the company releases its 2022 annual financial statements before the local stock market opens on 24 March 2023, positive surprises are more likely than negative ones.

Capital measures

The company initially intended to raise CHF 20 million through its most recent bond issue. However, demand turned out to be so strong that the company ended up raising capital of CHF 34.7 million. This bond has a coupon of 3% and matures in 2026. By contrast, a capital increase of CHF 150 million approved by the AGM in April 2022 was postponed in July, as cash inflows from project sales were deemed to be more attractive for shareholders.

Summary

A look at the price performance of Edisun Power shares over the longer term reveals an all-time high of CHF 166 in August 2019, followed by a low of CHF 90 in March 2020. The stock has broadly traded sideways ever since, oscillating around the CHF 120 mark as the rough median line. Interim lows have been more pronounced than interim highs, with the ultimate result being a horizontal wedge shape. Once the end point of this trend is reached, the stock will have to break out in one direction or the other.

There are good reasons to think that 24 March 2023 could be the moment at which the shares will embark on an upward trajectory. Given the company’s strategy changes and its focus on accelerating the growth of sales, earnings and the dividend, opportunity-seeking investors are likely to adopt a more favourable view of Edisun Power. The stock could also benefit more in the future from the decarbonization measures being implemented by institutional investors as they look to reduce the CO2 intensity of their portfolios. What’s more, with an estimated P/E ratio of 10 to 12 for 2022 and a potentially much lower P/E ratio in 2023 and the years thereafter, the stock looks attractively valued. If the payout ratio remains the same, investors can also expect to enjoy significant dividend increases in the new era of the company’s development.

Relative to comparable listed solar companies, Edisun Power appears to be undervalued. The planned sale of projects could deliver exceptional profits in the three-digit million area in the period 2023 to 2025, i.e. more than the current market capitalization of around CHF 120 million implies. As a small cap with very low liquidity – the free float currently stands at just 38% – the stock has so far attracted little attention. But that could rapidly change in the event of earnings rocketing skywards.