The future is electric! And if climate targets are to be achieved, the process of electrification will have to unfold much more rapidly than it has done to date. This is true of mobility concepts, energy generation and storage, industrial production, and a great deal more besides. Schaffner Holding is a global market leader with very specific expertise in the area of electrification. So what are the chances of this stock now experiencing an initial jolt that will awaken it from its 20-year slumber?

Without electrical devices, our modern society would be in a pretty pickle. From ovens to computers, from industrial automation to medical equipment – almost everything is driven by electricity. Ever since the era of Albert Einstein, it has become clear to mankind that light, electricity and magnetism are different manifestations of one and the same thing – electromagnetic waves. The use of electricity as a means of lighting and as a supply of energy to industry and households is now so widespread that it is impossible to imagine life without it, but in fact the history of global electrification did not really take off until the 1880s, in the wake of the industrial revolution.

Electromagnetism

On the one hand, the Earth’s strong natural electromagnetic field protects our planet from cosmic rays and bombardment from asteroids, but on the other electromagnetic fields can also be damaging and disruptive. The protection of living beings as well as systems and devices from electromagnetic radiation is regulated and monitored by various national and supranational institutions. Electromagnetic compatibility – or EMC for short – describes the ability of electrical devices to function expediently when faced with very different requirements and parameters, rather than interfering with themselves (or indeed each other).

Electromagnetic compatibility

This is precisely the core competence of Schaffner – a global market leader in electromagnetic compatibility. The various filters and chokes ensure the flawless functioning of electrical systems with no disruption – be it in a car, magnetic resonance tomography, a «smart» building, or energy production and storage.

Founding

The company was founded in 1962 by the eponymous Hans Schaffner. To start with it produced heat dissipaters and electronic relays. International expansion began in 1975 – initially to France, and then to Germany and the US. The company was acquired by Elektrowatt in 1981, but its expansion continued.

Change of ownership

The company underwent another change of ownership in 1996. Management and financial investors acquired Schaffner through a management buyout (MBO). The company then floated on SIX in 1998. The following years saw a number of further takeovers, but later also various divestments. Fast forward to today and Schaffner primarily manufactures EMC filters, harmonic filters, transformers, and other products for the hitch-free functioning of electrically operated systems, machinery, apparatus, and devices.

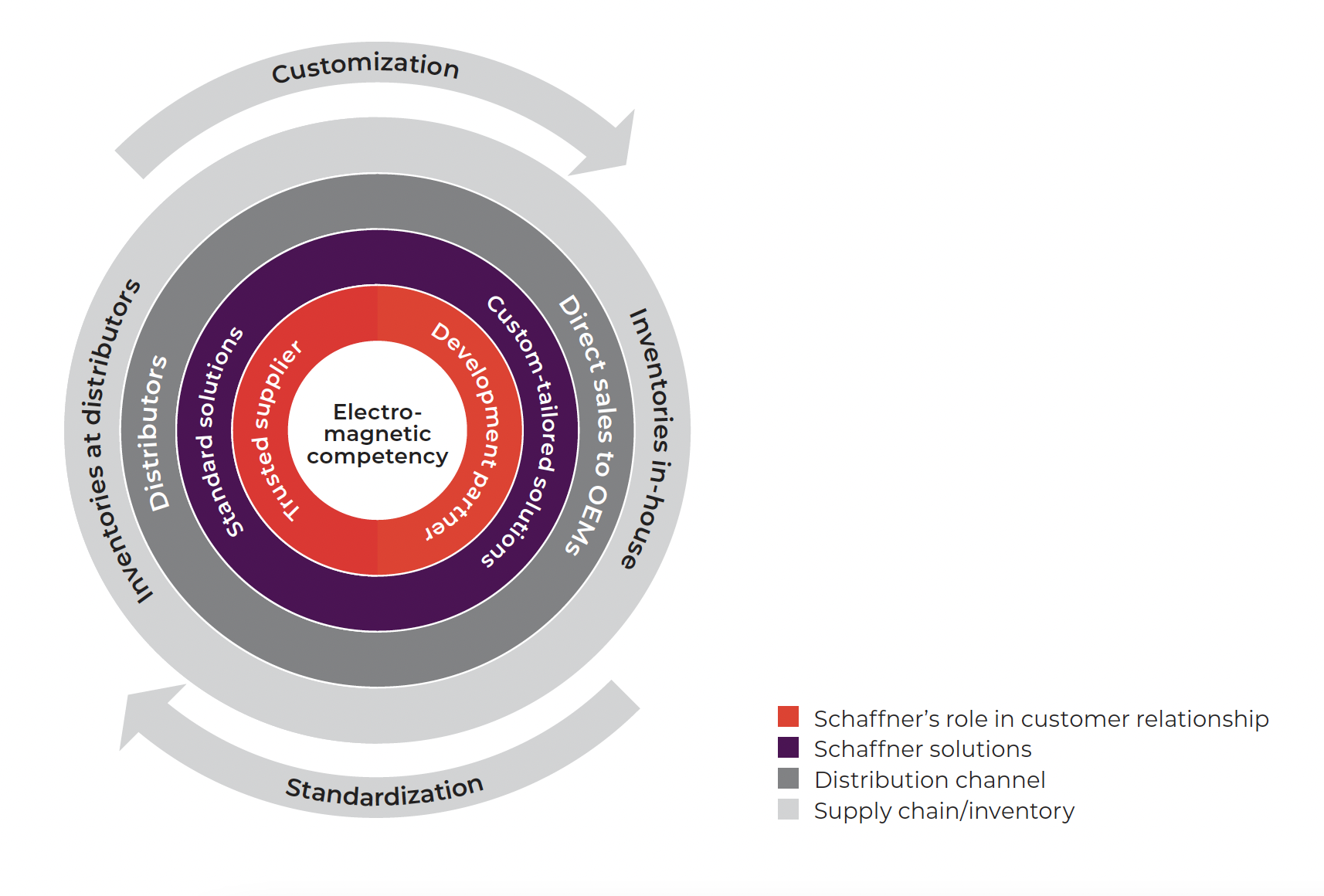

An electromagnetic moat

The key markets serviced by the company are machinery and robotics, building technology, energy management, the automotive industry, medical technology, as well as data and communication. Unlike most other companies, the usual starting point of interaction between Schaffner and a customer is the development of one or more customized solutions in line with the latter’s specific requirements. The findings obtained through this process then feed into the company’s standard products, which are also distributed by various partners. These standard products – which are typically also the market standard – provide higher margins. Thanks to this rather unconventional business model and its continuous flow of innovations, market leader Schaffner can also push through price increases, particularly as competition is thin on the ground. This often prompts OEM customers to neglect EMC issues or pursue their own solutions, but these attempts have a high failure rate, and so customers come back. Indeed, it would not be exaggerating things to say that Schaffner has an “electromagnetic moat”, which neither its competitors nor any other powerful corporate groups appear able to bridge.

Electrification 2.0

The company’s various target markets may be different, but they exhibit similar characteristics. In all cases, customers are looking for technologies and products that cut costs, reduce and efficiently manage energy consumption, and decrease or even eliminate the emission of damaging greenhouse gases. The technological expertise possessed by Schaffner is just as relevant for renewable energies as it is for energy production and transfer involving fossil fuels. In the area of electro-mobility, which is now on a steepening growth trajectory, EMC filters are gaining in importance compared to conventional vehicles. EMC filters are also essential in the world of decentralized energy storage and distribution through «smart grids». Even buildings are built out of more than just conventional construction materials nowadays – they also have to be «smart», i.e. optimally networked, monitored, and fitted with intelligent systems to control ventilation, air conditioning and heating, as well as elevator systems.

Changed priorities

Energy efficiency and climate neutrality have now become overarching priorities in all markets. The pace of change has also picked up significantly since the start of the war in Ukraine a year ago, as «energy autarky» has now suddenly taken on a whole new significance. With all its various elements, this accelerated structural change is unleashing a growing surge in demand in areas of the economy that are affected by the ongoing process of electrification.

Surge in demand

According to Bloomberg, the financing of energy transition in Germany alone will require a staggering EUR 1 trillion to be invested by 2030. One example is the requirement for increasing numbers of fast-charging stations for electric vehicles. Here the specific EM filters produced by Schaffner are of crucial importance. All markets serviced by Schaffner are system-critical in the broadest sense, which is why we are in all likelihood witnessing not simply a short-term spike in demand but the beginning of a structural growth surge – and one that can be expected to persist for many years to come.

High order intake

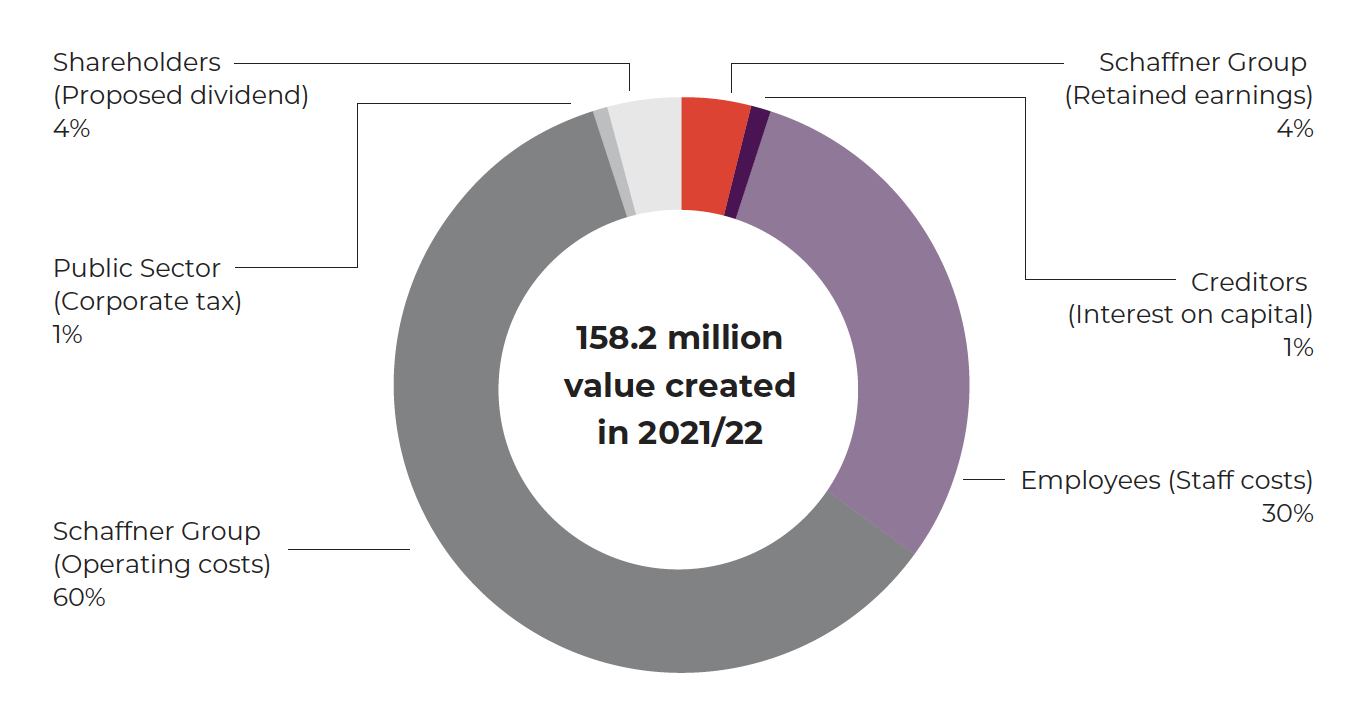

This can already be gleaned from the company’s most recent financial statements for the year ending 30 September 2022. The order intake was a good 10% higher than annual sales, resulting in a book-to-bill ratio of 1.1. After adjusting for the divestment of one business area, sales for the 2021/2022 financial year rose by 7.4% to CHF 158.2 million. Sales growth in local currencies was as much as 10.5%. The strongest performer was the Industry segment, which recorded an 18.3% rise to CHF 128.5 million. By contrast, sales in the Automotive segment declined by 23.1% to CHF 29.7 million. Although several new OEM customers in the area of electro-mobility were acquired, this could not compensate for weaker demand from manufacturers of conventional vehicles. EBIT amounted to CHF 15.4 million, equivalent to a margin of 9.7%, although this then rose to 10.5% at the end of the financial year as a result of price increases. Net profit came in at CHF 12.6 million, resulting in an impressive net profit margin of 8%. Earnings per share amounted to CHF 19.99, with the dividend unchanged at CHF 9.00 per share. At the current stock price of CHF 266, the historic P/E ratio for 2022 works out at a 13.3x, while the dividend yield amounts to 3.3%.

Triple bottom line

Schaffner’s vision is to contribute to a «sustainable and electrified society». Its mission is to deliver EM solutions for the efficient, reliable and sustainable use of electrical systems. The company also makes reference to its «triple bottom line», comprising people, planet, and profit. In keeping with this expanded objective, Schaffner has for the first time drawn up and published a Sustainability Report for the last full financial year. At 86 pages this is quite substantial, and among other things sets out the various guidelines which the company is committed to following – such as the 17 SDGs of the UN and the UNGC Principles.

ESG track record

But how credible is this drive to establish the company’s credentials in the area of sustainability? Photovoltaic facilities have been installed at the company’s new headquarters in Switzerland, as well as at its production site in Thailand. Employees have been incentivized to switch to electric vehicles or bicycles. Schaffner’s vehicle fleet is also being converted to electric vehicles. The CO2 emissions of the company’s own vehicles were reduced by 52% last year. Overall emissions declined by 35% in the last financial year, while energy consumption was down 25%. Employees wanting to travel on business now need to provide compelling reasons, and the CO2 emissions associated with these trips accordingly declined by 43% last year. Also notable in the ESG sphere is what did not happen last year: no fatal accidents and only two workplace injuries, no cases of corruption, violation of human rights, or child labour were identified, and no data leaks or data losses were recorded.

Diversity

Of the company’s workforce of 1,800 (of which 46% are women) more than 1,400 employees work in Thailand, a further 200 in China, and 100 in Switzerland. No less than 13 nationalities work side by side in Switzerland. The company is proud of its cultural diversity. This is particularly true in Thailand, where Schaffner is a partner to the strong local LGBTQ community. LGBTQ employees regularly add a dose of spice to numerous festivities such as the Schaffner Idol Contest.

Transparency

Transparency and corporate citizenship are now basic prerequisites if a company wants to remain attractive to employees, customers, and investors. Schaffner’s most recent set of figures shows that far from coming at the cost of profitability, these attributes actually enhance it. CHF 46.8 million was distributed to employees, CHF 5.7 million was passed on shareholders, while CHF 1.8 million was paid to the tax authorities. The retained profit of CHF 6.9 million will secure the company’s freedom of manoeuvre going forward.

Summary

The enormous growth potential presented by the acceleration of electrification is not just an abstract concept – it is being driven by numerous initiatives, programs, and micro-decisions on the part of the various economic actors. But what is new here is the momentum of change. For too long, value creation has been built on cheap fossil fuels, which we now know is not just a climate killer but also a strategic disadvantage in the changed geopolitical landscape since 2022. The challenge for mankind now is not just to rapidly expand the energy mix and tilt it emphatically in favour of renewable energies, but also to increase electricity production capacity significantly. Electric vehicles, heat pumps, and exponentially rising data streams will provide substantial demand stimulus.

It is difficult to see anything that could prevent Schaffner from benefiting from the competition of Electrification 2.0 comprehensively, and in a lasting way. Against a fundamentally changed backdrop, longer-term growth in demand could prove well above Schaffner’s target of 5% annual growth. The company’s guidance for the EBIT margin is a bandwidth of 10–12%. The valuation of Schaffner, which has been highly profitable recently, is very appropriate for a cyclical company, which is essentially what Schaffner has been for the last 20 years. But it is too low for a company that possesses system-critical technology in a structural growth market. Its shareholders are in good company: The free float stands at 41%, while the Buhofer family holds 17.2%, and other long-term shareholders and asset managers such as UBS and Mirabaud hold the remainder.