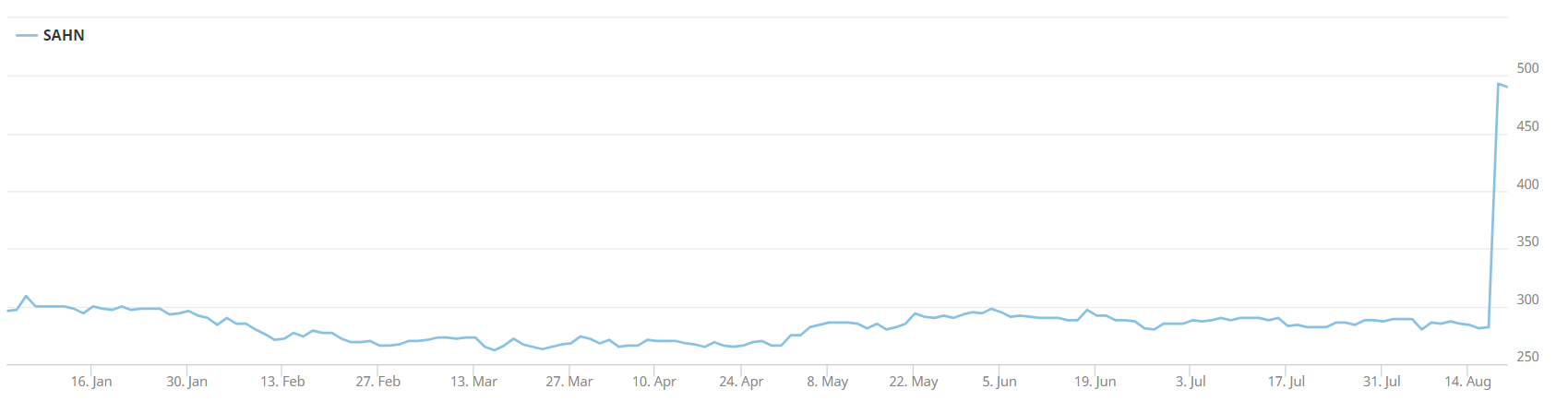

There was not much market interest in Schaffner Holding on 16 August. Indeed, just 171 shares were traded at a price of CHF 282. But just a day later, the NYSE-traded but Schaffhausen-domiciled company TE Connectivity announced a public takeover offer for all outstanding shares. The price? A stunning CHF 505 per share.

The premium to the last-traded price on the previous day works out at 79.1%, and is still a whopping 74.5% when based on the volume-weighted average price of the last 60 trading days. This is the kind of takeover premium that most investors can only dream of. An obvious comparison that springs to mind is the only recently announced takeover of the traditional industrial company Von Roll by Germany’s Altana. However, in the case of this micro-cap, the premium offered to the last-traded stock market price works out at just under 10%, with Altana’s takeover offer valuing Von Roll at CHF 307 million.

Comparison with Von Roll transaction

Another key difference is the ownership structure. In the case of Von Roll, the heirs of the von Finck clan are clearly keen to cash in on their investment. Between them they effectively hold a stake of 84.3%, and there is clearly no desire on their part to wait and reap the fruits of the nascent turnaround. The case of Schaffner is rather different. The new growth stimuli coming from e-mobility, alternative concepts for the energy economy, connectivity, and electrification 2.0 are already clearly feeding through into the figures. In particular, the last few years have seen a sharp increase in profitability.

Surge in growth and earnings evident at Schaffner

As per 31 March 2023 – i.e. at the end of the first half of the current financial year – Schaffner’s EBITDA margin had reached 16%, and its EBIT margin 12.6%. Earnings were up 89.8% on the prior-year period, coming in at CHF 9.8 million, which equates to CHF 15.48 per share. Based on a market capitalization of CHF 180 million, the annualized P/E ratio prior to the takeover offer therefore stood at less than 10x. As already pointed out in March in the article “Schaffner Holding: Who can bridge its electromagnetic moat?”, such a valuation might well be appropriate for an “old school” industrial company exposed to the cyclical ups and downs of the economy, but not for a market and innovation leader whose products and expertise are indispensable to the majority of industries of the future. In a structural growth market with exponentially increasing growth rates, a higher valuation for such a company with expanding profit margins is only appropriate.

Efficient market theory?

However, investors in the Swiss equity market clearly did not appreciate the strong operating developments unfolding at Schaffner. The return on capital employed (ROCE) most recently stood at a handsome 33.5%. The equity ratio of 68.6% is likewise impressive. Nonetheless, the undervalued stock remained largely illiquid, with the price continuing to oscillate sideways in a narrow price bandwidth. Whether investors lacked imagination, or whether it was a case of the micro-cap Schaffner (with a market cap of just CHF 180 million) not even being on their radar, is not clear. Perhaps both points are true. But what is clear is that equity pricing in the markets away from the large caps remains far from efficient, for all that this mantra has been trotted out on numerous occasions. Schaffner also appears to have attracted no great attention from the numerous small-cap and mid-cap funds.

Buyer profile

Market inefficiencies of this kind offer genuine opportunities for stock pickers, value investors, contrarians, financial engineers such as private equity investors, and of course industrial players whose actions are underpinned by “industrial logic”. TE Connectivity, known as Tyco Electronics up until 2011, clearly falls into this latter category. Over the last five financial years, its sales have risen from USD 14 billion to USD 16.3 billion, albeit with fluctuations. Earnings amounted to USD 2.4 billion in 2022. The company is a competitor of Schaffner in the area of electromagnetic filters, where it is the fourth-largest player when ranked by global market share. In the most recent quarter ending as per 30 June, the EBITDA margin worked out at 22.4%. The company’s main business consists of sensors and connectivity solutions aimed at the same industries serviced by Schaffner.

Big dog eats smaller dog

TE Connectivity’s market cap currently stands at USD 40 billion. If either sales or profitability is taken as the yardstick, TE Connectivity is around 100 times larger than its takeover target. However, the former’s market cap is more than 200 times that of Schaffner. Quite aside from the superior strategic positioning it will achieve as the global number one in the EMC filter segment, this transaction makes sense from the buyer’s perspective because it exploits the valuation difference to the larger company’s advantage – even allowing for the hefty premium being paid.

Major shareholder supports takeover offer

TE Connectivity is happy to pay this strategic premium. According to Schaffner CEO Marc Aeschlimann, the acquiring party first approached Schaffner in the spring of this year. The company’s largest single shareholder – Buru Holding, representing the Swiss entrepreneur Philipp Buhofer, with a stake of 17.2% – is supporting the takeover offer. In addition to tendering all its shares, it will also be recommending that other shareholders accept the approach. The other significant shareholders are the asset managers J. Safra Sarasin with a stake of 9.8% and UBS Fund Management with a stake of 9.1%. The remaining 63.9% is held by other shareholders. This was the finding of the audit company EY, which was commissioned to carry out a company valuation of Schaffner Holding.

Illiquid micro-cap

For regulatory reasons, a valuation of this kind by an independent audit body was necessary: According to the regulations of SIX Swiss Exchange, Schaffner stock is classified as an illiquid micro-cap, as the relevant liquidity threshold (minimum monthly trading volume of 0.04% of the free float) was not reached in 9 of the last 12 months. For a company to avoid such a classification, this liquidity threshold needs to be exceeded in at least 10 of the past 12 months. If this criterion is not met, any takeover must be accompanied by an independent expert valuation.

Independent company valuation by EY

The corresponding report can be found at https://emc-power-offer.com/websites/3003_ma/English/1000/announcements.html. This is a company valuation based on a combination of historical data and interviews with management. No due diligence or formal audit under Swiss stock company law was conducted, nor did the valuation attempt to identify any synergy potential. Based on plausible assumptions, the experts of EY calculated the value of Schaffner on the basis of various standard financial industry valuation procedures, first and foremost the DCF method. In addition, sensitivity analyses were carried out and the trading multiples of comparable companies as well as transaction multiples for similar takeovers were scrutinized. In the final analysis, EY determined the minimum value per share as CHF 336.40.

Minimum value of CHF 336.40

However, the bandwidth of valuations arrived at through the four complementary methods is very wide. The highest value came in at CHF 507.1. This corresponds to the highest trading EBITDA and EBIT multiples of the international peer group. The lowest value based on this valuation method amounts to CHF 339. The DCF method requires assumptions to be made for the future. In two scenarios, EBITDA margins of 16% and 18% were calculated up to 2027. The valuation bandwidth here ranges from CHF 269.40 to CHF 403.40. In the case of transaction multiples, the lowest value works out at CHF 242.10, the highest at CHF 341.80. But whatever calculation method is adopted, the proposed takeover price of CHF 505 is well above the valuations of the independent expert. This figure also just happens to correspond to the highest price recorded by Schaffner stock since 2001.

Timeline

The offer prospectus is due to be published on 28 September, with the tender period starting around two weeks later. The aim is for the transaction to be completed by December. However, if this is to be achieved, the necessary official approvals will have to be granted. Schaffner stock is currently trading at the level of CHF 490, reflecting the typical discount of a target stock in the run-up to a takeover.

Summary

This transaction has a number of aspects. For CEO Marc Aeschlimann it represents a success and a source of “personal satisfaction”, to quote his own words in a recent interview. But it is very much a success for shareholders too, as ultimately the value of this stock has risen by the eye-popping amount of almost 80% overnight, to a 22-year high. It is also a positive development for employees, whose future prospects look all the brighter as part of a strong conglomerate. Market growth and synergies open up all sorts of new potential. As of the most recent reporting date, the US accounts for just 14% of Schaffner sales.

The flipside of the coin is that the Swiss market is losing a global market leader with significant growth and stock price potential. And although SMEs such as Schaffner play an important role in the economy, their value is typically little appreciated by the stock market or even ignored altogether by certain groups of investors. There are of course exceptions to this rule, such as the on-trend examples of the “hot” stocks Asmallworld, ASM and Meyer Burger. In an efficient market, the price of Schaffner stock would probably have long since caught the attention of more investors and risen to a higher level. It is likely that we will see further takeovers and “go-private” transactions of SMEs while the market permits such a striking divergence of value and price, as it did for Schaffner.